Testimony of the Vermont League of Cities and Towns

Ted Brady, Executive Director

to the Senate Committee on Government Operations

Regarding H. 629

April 3, 2024

My name is Ted Brady, and I am the Executive Director of the Vermont League of Cities and Towns, which represents all 247 cities and towns in Vermont. I thank the committee for inviting me back to discuss H. 629, a bill that proposes to make significant changes to the tax sale process. If anyone missed my testimony on March 26th, I encourage you to review that testimony for a full understanding of VLCT’s position and concerns about this bill. Today I simply want to reiterate VLCT’s primary concerns that we’d like to see addressed in the bill:

- Section 4 creates a new personal service requirement. This exceeds the notice requirements recognized by both the Vermont Supreme Court and the U.S. Supreme Court and puts an onerous burden on municipalities. Personal service is costly, and these additional, unnecessary, costs will be added to the delinquent taxpayer’s debt.

- Section 6 cuts the interest rate from 1% to 0.5% for investors that purchase properties at tax sale. This will result in fewer investors interested in bidding at tax sales, which forces municipalities to pay a higher share of delinquent property taxes to the state. This would place a further burden on taxpayers who do pay their property taxes on time and would take away tools that help municipalities collect delinquent taxes. Will the state forgive property taxes owed by municipalities because of not being able to collect them due to these new tax sale requirements? It also eliminates language that calculates interest for partial months.

During my last visit to this committee, several members of the committee asked if VLCT had any data on how many tax sales are occurring. VLCT is currently conducting the Municipal Data Project, a year-long effort to gain and analyze information about municipalities. As part of our first data gathering effort in this project, we did receive some data on tax sales and abatement that I wanted to share.

Seventy-seven cities, towns or villages responded to VLCT’s municipal finance questionnaire that included several questions related to delinquent taxes and tax sales. Of the 77 municipalities, here is some of the raw data:

- Towns used a variety of Delinquent Tax Collection options; including tax sales, graduated payments, grace periods, payment plans, waived & reduced late penalties, and foreclosure/civil action.

- Other interesting data points:

- Of those municipalities that responded there is over $8.5M in delinquent taxes owed.

- Many towns have had no tax sales but have over $250,000 in delinquent taxes owed. - 42% had no tax sales and 40% had at least one tax sale between 2021 and 2023 (Note: the remaining survey respondents skipped the question)

- Of the 101 tax sales that the 70 municipalities reported over those three years, properties were redeemed on average 56% of the time (32% in 2023, 81% in 2022 and 55% in 2021)

The chart below shares the aggregate values of properties that went to tax sale (as reported by the 70 municipalities reporting property tax sales between 2021 and 2023) vs the aggregate tax sale amount.

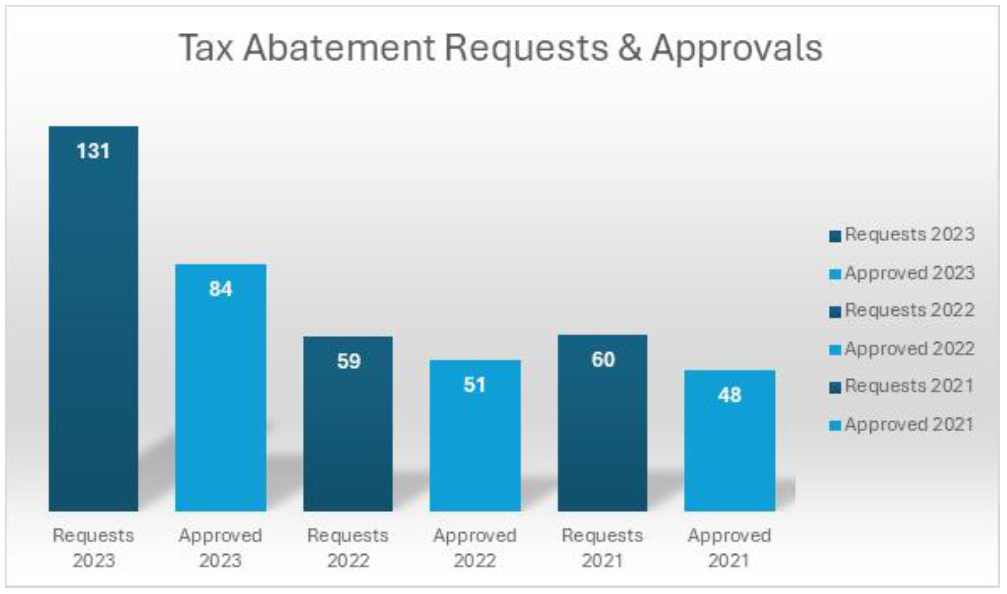

As the chart below shows, 33 of the 77 respondents said they received property tax abatement requests between 2021-2023. Below is a comparison of the abatement requests received vs. abatement requests approved.