Testimony to the Senate Government Operations Committee

and the Senate Finance Committee

Regarding Flood-Related Municipal Financing (H.397)

Josh Hanford, Director of Intergovernmental Affairs, VLCT

Samantha Sheehan, Municipal Policy and Advocacy Specialist, VLCT

April 11, 2025

Good Government: VLCT/VBB Suggested Amendments Related to Municipal Finance

Given the various unique charter authorities in some communities, these provisions are most likely to help rural towns.

These proposals have been broadly socialized across the legislature this session and are well received. Other committees where we have testified include Senate Appropriations, Senate Government Operations, and House and Senate Transportation.

They are supported by VLCT, Vermont Bond Bank, Clerks and Treasurers, School Business Officials, and Governmental Finance Officials, and UAFB is recommended by numerous auditors.

All together, these provisions will improve emergency responsiveness for municipalities, create new, stabilizing factors for local property taxes, and will improve grant readiness for towns and cities as we approach a potentially volatile period for federal funding.

July 10, 2024 Municipal Flood Damages

Examples of outstanding emergency debt pending FEMA reimbursement:

Lyndon: $15M (x2 the town budget)

Moretown: $8.25M

Middlesex: $7M (x3 the town budget)

Cavendish $1.6M

Barnet: $1.5M

Bridgewater: $3M (2x the town budget)

Of the municipal entities impacted by the 2024 floods, one third (1/3) make up 91% of the total estimated damages.

Two thirds (2/3) of the municipalities impacted were also impacted in July 2023, and 64% of those are towns with a population less than 2000.

Approaches to Funding Flood Resiliency

Financing strategies must be paired with appropriate technical assistance for grants management and municipal finance, and with expanded municipal authorities to exercise best practices for government finance.

- Grants are competitive and require local matches

- FEMA reimbursement is complex and time consuming

- Through MTAP, VLCT continues to assist 2023 and 2024 flood affected towns to manage their flood debts, grants, and reimbursements. VLCT provides this assistance through direct, one-on-one assistance to municipal officials (free to the towns) as well as through workshops and online resources. Over 200 registrants have joined these online flood related trainings.

Section 10: Unassigned Fund Balance

We recommend action to allow municipalities to employ the prudent fiscal practice of providing for unassigned fund balance within the municipal general fund budget.

Establishing an Unassigned Fund Balance would:

assist in cash flow management

stabilize the tax rate

improve emergency response

significantly strengthen municipalities' financial resiliency in the case of unexpected negative economic trends

improve grant readiness by making flexible monies available

improve the municipality's borrowing position, saving taxpayers money on the cost of municipal debt.

Section 11: Emergency Borrowing

VLCT and the Vermont Bond Bank request a new authority to borrow for up to a five-year repayment period in the case of an all-hazards event.

Vermont municipalities have become increasingly familiar with complex and extensive processes required to access emergency funding and FEMA Public Assistance.

In the wake of flooding and major weather events, municipalities cannot wait to rebuild vital town infrastructure or to restore municipal services.

State law substantially limits the authority of local legislative bodies to acquire funding for emergency response as they can only take on debt for up to one year without a town vote.

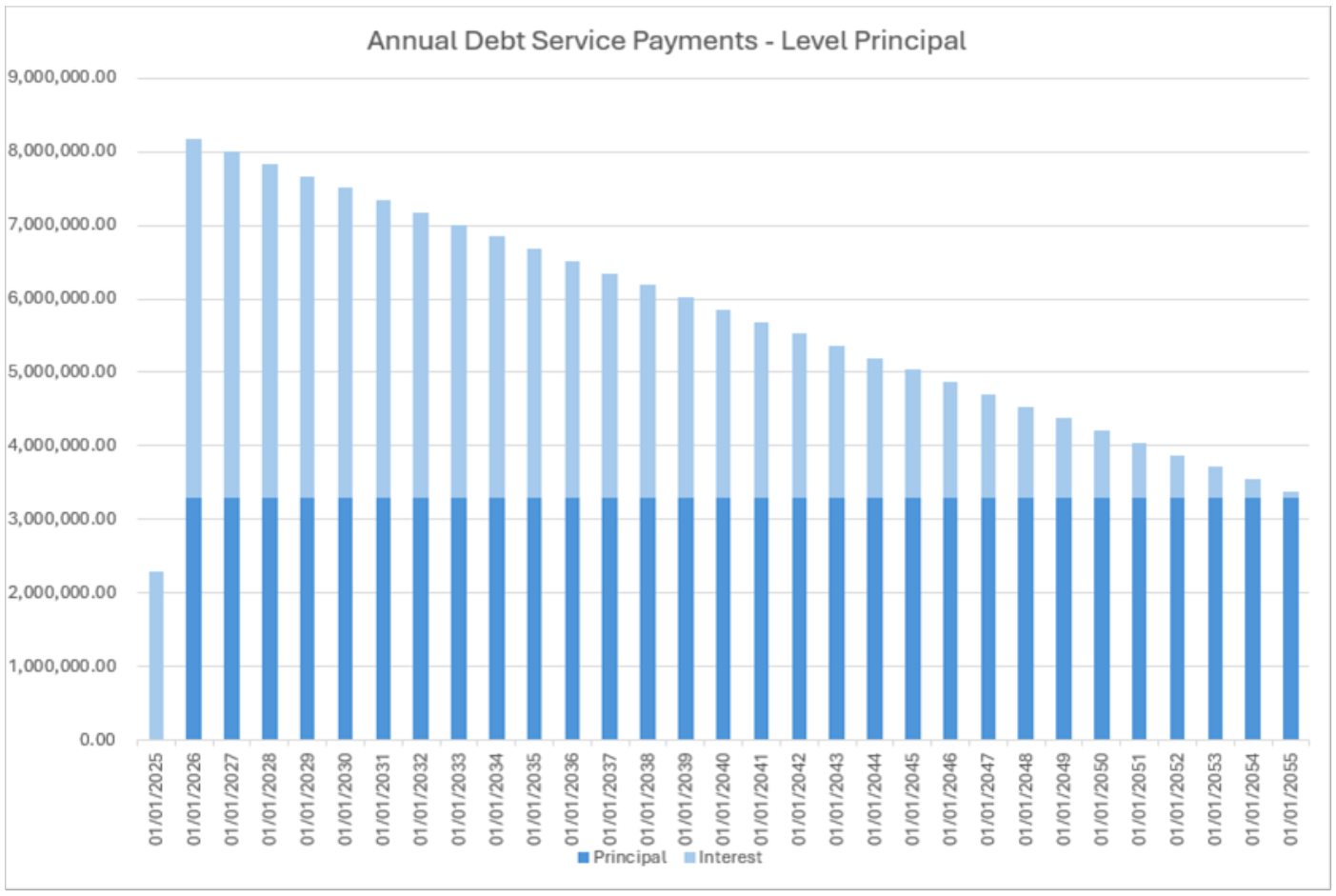

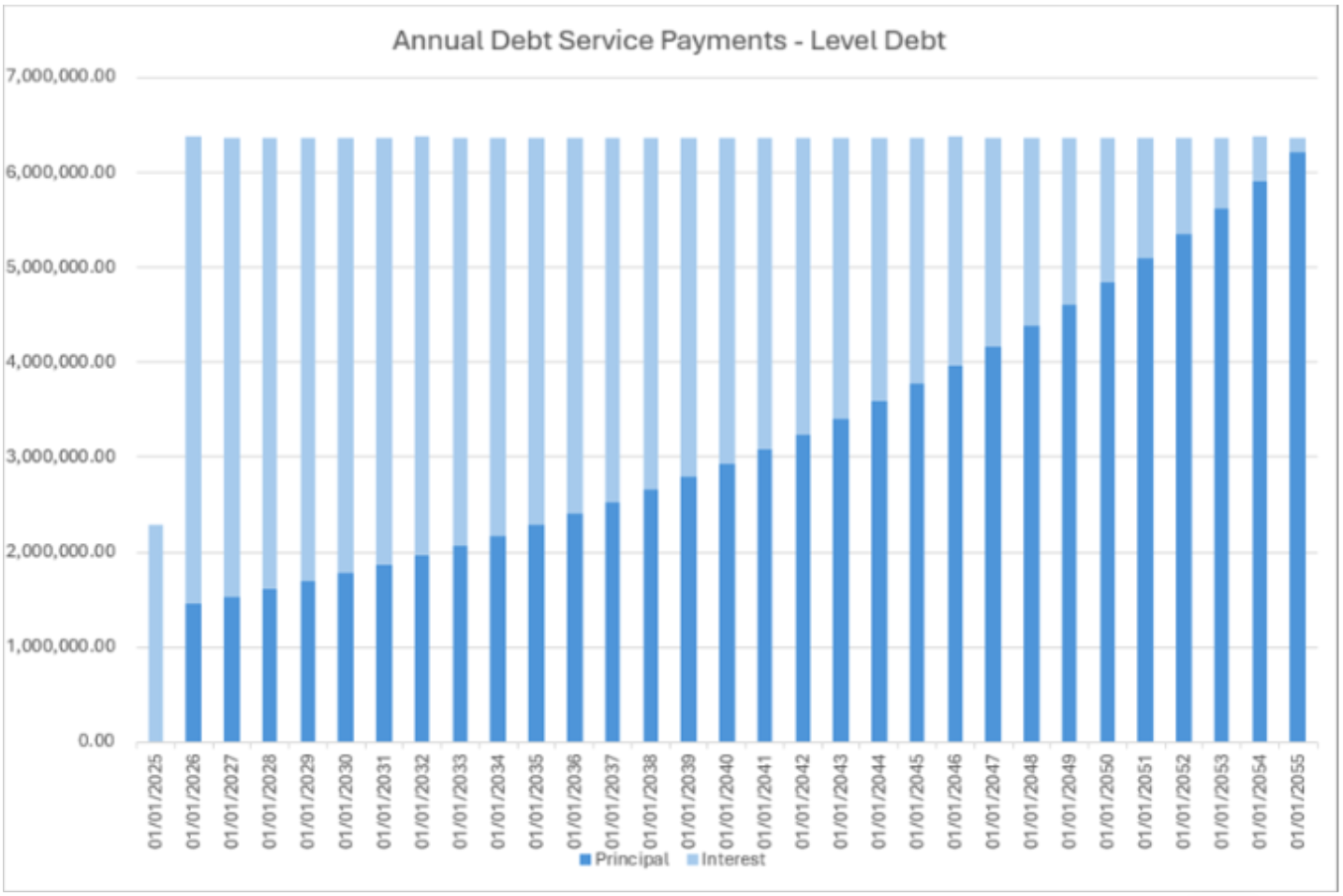

Proposal: Level Debt Service

To improve predictability for municipalities and for taxpayers, VLCT and the Vermont Bond Bank request a change to allow for flexibility in bond repayments to include level debt option. Members of the Vermont School Board Association and Superintendents Associations have also expressed support for this change.

Current statute requires municipal loans to be level principal.

Debt payments for level principle borrowings start high and decrease yearly as the cost of interest goes down.

Municipalities should have the option to structure level debt or level principle.

This is more within the norms of government borrowing nationally.

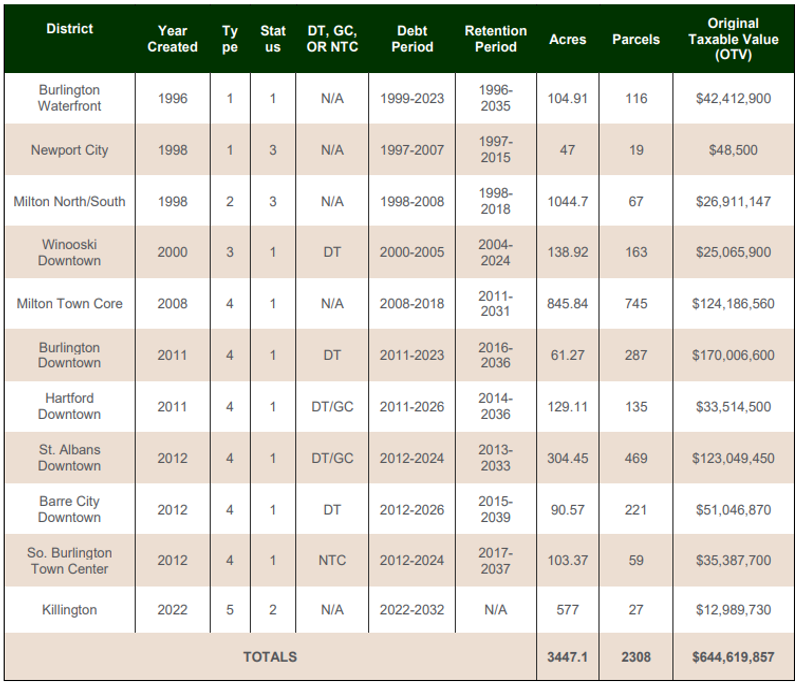

Level Debt Service and TIF

Of the 11 TIF Districts, only 9 are active. Only Hartford and Barre could leverage level debt service within the TIF through 2026 and only Killington beyond 2026. Killington is projected a 2277.63% increase in taxable value, providing ample capacity within the new district to responsibly manage debt.

- The debt capacity of the TIF is regulated by VEPC.

- The municipal debt authority requires voter approval, including "Estimated amount and types of financing that will be serviced or paid using District increment, including principal, and estimated interest, and fees, and terms of the debt."

- Revenues from the original taxable value is retained by the Education Fund and Municipality respectively, plus a portion of tax increment revenue to the Education Fund.

Section 13a: Local Option Taxes:

VLCT Supports an Amended Withholding Ratio of 80/20

- Through FY25, 34 municipalities have acted to adopt LOT and at least 4 municipalities approved one or more LOT at their 2025 Town Meeting

- With the proliferation of short-term rentals and online commerce, an increasing number of municipalities may benefit from LOT.

- Presently, all 34 LOT communities established this taxing authority through a charter process and most have obligated these revenues to support a range of local initiatives.

- There is a long history of legislative actions to revise the LOT program. Act 60 of 1997 authorized LOT for a limited time at 60/40. Various Acts extended the sunset and modified criteria for municipalities. Act 215 of 2005 established the current 70/30 split of LOT revenues between municipalities and the PILOT Special Fund and removed the sunset. In the 2024 Miscellaneous Tax bill, non-chartered municipalities were granted the authority to adopt LOT.

Section 5: Flood Buy-Out Program

- VLCT's 2025-2026 Municipal Policy includes: Ensure ongoing funding for the state flood impacted property buy-out program including relocation and rebuilding of municipal properties in flood danger.

- 51 municipalities have at least one buy-out property

- Nine out of the 34 LOT municipalities have at least one buy-out property and several are PILOT eligible including Barre, Montpelier, Berlin, and Waterbury

- A $1M appropriation should be adequate to compensate the municipal portion of lost property taxes due to buyouts for all 51 municipalities for a period of five (5) years.

Proposal: PILOT Special Fund Surplus $10.3M and Growing

The PILOT Special Fund revenues are local revenues, created by a process of local control. In consultation with the current 34 LOT towns, VLCT advocates that the majority of current surplus monies should be returned to those communities which generated the revenues.

- The surplus is driven by a growing list of municipalities choosing to add LOT and quickly growing consumption tax receipts, which are up about 44% since the pandemic.

- At the end of FY24 the fund carried a $10.3M surplus and is likely to generate a nearly $4M surplus in current FY25.

- On Town Meeting Day 2025: Ludlow, Marlboro, Montgomery, and Montpelier all approved new LOTS which projected to add about $530,000 to the fund in FY26.

- In order to prorate PILOT payments at 100%, a moderate surplus should be maintained in the special fund.

- If no appropriations were made other than PILOT, and the LOT ratio stayed at 70/30, the FY26 end of year surplus would be about $14,830,000

Example Surplus Appropriation

Assuming FY26 PILOT Appropriations ballpark $12,130,000 ($500K over FY24)

| Option A: Reserve 15% Surplus | Option B: Return FY24 Surplus only | ||

| Projected FY26 PILOT Surplus | $14,380,000 | Projected FY26 PILOT Surplus | $14,380,000 |

| Minus Reserve for Flood Buyout Municipal Tax Reimbursement | $1,000,000 | Minus Reserve for Flood Buyout Municipal Tax Reimbursement | $1,000,000 |

| Return Surplus balance to 34 LOT Municipalities | $12,010,000 | Return FY24 Surplus to 34 LOT Municipalities | $10,300,000 |

| 15% PILOT FY26 Surplus retained | $1,820,000 | 25% PILOT FY26 Surplus retained | $3,080,000 |